AI Reskilling in Accounting: Why Lived Experience Matters More Than Metrics | Dr. Ammar Ashour

Dr. Ammar AshourHomeServicesInsightsContactHome › Insights › AI Reskilling in Accounting

Doctoral Research · Methodology

Firms are deploying AI in tax, audit, and reporting faster than they are preparing the people who have to work alongside it. Here is why my doctoral study listens to accountants instead of measuring them.

AA Dr. Ammar M. Ashour, DBA CandidateApril 18, 202612 min read

The accounting profession is absorbing artificial intelligence faster than it is preparing the people who have to work alongside it. Generative tools are drafting memos. Automated audit analytics are flagging anomalies. Machine learning is reshaping tax and reporting workflows. And the pace of deployment is outrunning the pace of structured, human-centered reskilling.

That imbalance is not an operational problem. It is a human one. It changes how accountants experience their own productivity, how they feel about the work they are doing, and how confidently they navigate the ethical decisions that AI now drops in their laps every week.

Most of what we currently know about AI in accounting is told from the outside — firm-level performance dashboards, labor-market forecasts, and conceptual models produced by people who are not the ones doing the work. My dissertation is built on a different premise: if you want to say something useful about reskilling, you have to hear accountants describe the transition in their own words.

Reducing lived experience to a satisfaction score is like auditing a company by counting its office chairs. You get a number. You do not get the truth.

The Purpose of This Study

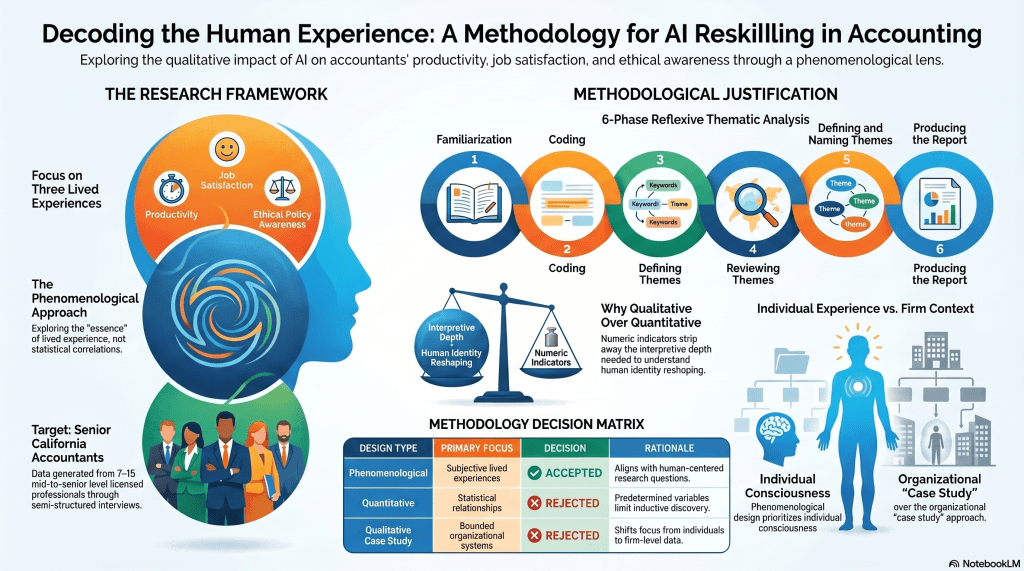

This is a qualitative phenomenological study of the lived experiences of mid-to-senior-level licensed accountants in California who have participated in firm-sponsored AI reskilling programs. The study focuses on three dimensions that matter to practitioners and partners alike: perceived productivity, job satisfaction, and ethical policy awareness.

Because the research questions ask what these experiences are — not how strongly they correlate with external outcomes — the methodology is oriented toward interpretive depth rather than statistical generalization.

Why this matters Firms that treat reskilling as a training checklist miss the point. Reskilling is a shift in professional identity. It is only visible when you stop measuring it and start listening to it.

The Three Research Questions

Everything in the design flows from these three questions. They are deliberately phenomenological — they ask about experience, not effect.

RQ1

Productivity

What are the lived experiences of mid-to-senior-level accountants who have completed firm-sponsored AI reskilling programs, particularly regarding perceived productivity?

RQ2

Job Satisfaction

What are the lived experiences of those same professionals regarding job satisfaction after reskilling?

RQ3

Ethical Awareness

What are their lived experiences regarding ethical awareness in AI-enabled practice?

The Research Design: Phenomenology with Reflexive Thematic Analysis

The study uses a qualitative phenomenological design with reflexive thematic analysis as the analytic technique. In plain language: I will sit down with accountants one at a time, ask them to describe their reskilling experience, and then look for patterns of meaning across all the conversations.

Phenomenology is specifically concerned with uncovering the essence of lived experience — the meaning people assign to a shared phenomenon, and the way that phenomenon shows up in consciousness. Because the research questions explicitly target lived experience, there is a direct methodological fit between the study’s purpose and its means of inquiry.

Who participates

Data will be generated through semi-structured, one-on-one interviews with a purposefully sampled group of 7 to 15 licensed mid-to-senior-level accountants in California who have completed firm-sponsored AI reskilling programs within the past three years. The interview protocol is organized around the three research questions, uses open-ended prompts, and incorporates reflexive probes that invite participants to articulate how training shaped their perceptions of productivity, satisfaction, and ethics in practice.

How the data is analyzed

Analysis follows Braun and Clarke’s six-phase reflexive thematic process — familiarization, coding, generating initial themes, developing and reviewing themes, refining and defining themes, and writing up — while I maintain a reflexive journal documenting analytical decisions, assumptions, and emergent interpretations.

Why This Design, Specifically

The justification rests on four reinforcing reasons.

One. Phenomenology aligns with the study’s epistemological position: meaning is intersubjective, contextual, and partial — not fixed or universally measurable.

Two. The design supports the interpretive depth required to capture the trust calibration, identity reshaping, and ethical reflection that accompany AI integration. None of those show up on a Likert scale.

Three. Reflexive thematic analysis is a strong analytic pairing with phenomenology because it generates patterned meaning across participants while foregrounding the researcher’s active interpretive role, rather than pretending to a posture of methodological neutrality.

Four. The design is congruent with the study’s theoretical framework, the Resource-Based View (RBV). RBV traditionally treats human capital as a credential; this study operationalizes it as an experientially developed capability. That reframing extends RBV into the subjective dimensions of reskilling outcomes — which is where the strategic value actually sits.

Three Alternatives I Considered and Rejected

Good methodology is not just the defense of a choice. It is the public reasoning behind three rejections. Here is mine.

| Design | Primary Focus | Decision | Rationale |

|---|---|---|---|

| Phenomenological | Subjective lived experiences | ✓ Accepted | Aligns directly with human-centered research questions. |

| Quantitative Correlational | Statistical relationships between variables | ✗ Rejected | Predetermined variables limit inductive discovery of meaning. |

| Mixed Methods (Convergent Parallel) | Triangulated quantitative + qualitative | ✗ Rejected | Adds instrument and sampling burden without proportional interpretive gain. |

| Qualitative Case Study | Bounded organizational systems | ✗ Rejected | Shifts focus from individual consciousness to firm-level data. |

Why not a quantitative correlational design?

A correlational design can measure the statistical relationship between reskilling exposure and outcome variables — productivity scores, satisfaction indices, ethics-awareness assessments. I rejected it for three reasons. First, the research questions ask about lived experience, not covariation. Reducing that to standardized numeric indicators strips away the exact content the study exists to capture. Second, the design cannot support the inductive, meaning-centered inquiry that reflexive thematic analysis enables, because it requires variables to be defined up front. Third, the target population — licensed mid-to-senior California accountants who have completed structured AI reskilling within the last three years — is specialized and geographically bounded, which makes the statistical power needed for correlational inference difficult to achieve.

Why not mixed methods?

A convergent parallel mixed-methods design collects quantitative and qualitative data simultaneously, analyzes each independently, and merges them at the interpretation stage. It is useful when both strands are genuinely needed to answer a research problem. Mine does not need both. The research questions do not require quantification. Adding a quantitative strand would dilute phenomenological focus without expanding explanatory reach. There is also recent methodological evidence that convergent designs frequently suffer from shallow integration, where authors juxtapose findings rather than genuinely synthesize them. For a single-researcher doctoral project with a focused California sample, the added instrument and sampling burden would compete with the interpretive depth that is the study’s whole point.

Why not a case study?

A single-firm or multi-firm case study could examine how AI reskilling unfolds inside specific accounting organizations. But the unit of interest in my study is the individual accountant’s lived experience across firms — not the firm itself as a bounded system. Case study logic privileges contextual embeddedness and triangulation across documents, observations, archival records, and informants; phenomenology privileges the distillation of essence across participants who share a phenomenon regardless of their organizational setting. Case study would also require firm-level access — documentation, process observation, multi-informant interviews — that is substantially harder to secure than recruiting reskilled individuals through professional networks, and that access could compromise the confidentiality that candid disclosure on ethics requires.

The bottom line The design I chose is not the only rigorous option on the table. It is the only one that stays aligned with what the research questions actually ask. Every other design would answer a different question well — just not this one.

What This Research Means for the Profession

This is more than methodological housekeeping. The choice to study AI reskilling phenomenologically is a deliberate argument that the accounting profession cannot understand its own transition using dashboards alone.

Firms investing millions in AI tooling and a fraction of that in human preparation are operating with a blind spot: they are measuring what is easy to measure, not what actually determines whether reskilling succeeds. The findings from this study are designed to fill that blind spot with the interpretive evidence partners and learning-and-development leaders need to build reskilling that works for the humans being reskilled.

Frequently Asked Questions

What is a phenomenological study, in plain English?

It is a type of qualitative research that tries to describe what an experience is actually like for the people going through it — not what it produces, not how it correlates with other variables, just the essence of the experience itself. The method is deliberately descriptive before it is explanatory. Who qualifies as a participant in this study?

Licensed mid-to-senior-level accountants based in California who have completed a firm-sponsored AI reskilling program within the past three years. The target sample is between 7 and 15 participants, selected purposefully to surface depth rather than demographic breadth. What is reflexive thematic analysis?

It is a six-phase analytic technique developed by Braun and Clarke: familiarization, coding, generating initial themes, developing and reviewing themes, refining and defining themes, and writing up. It treats the researcher as an interpretive instrument rather than a neutral observer, which is why it pairs so well with phenomenology. How does this research extend the Resource-Based View of the firm?

Traditional RBV treats human capital as a credential or certification — an asset the firm owns. This study reframes human capital as an experientially developed capability that accountants build through reskilling, which means its strategic value is not visible in HR records. It shows up in judgment, trust calibration, and ethical confidence. Where can I read the full dissertation?

The dissertation is in progress at California Southern University’s School of Business and Management. If you would like to follow the publication timeline or cite the work, reach out through the contact page on this site.

Need a consulting partner who understands AI and accounting?

A&A Tax Consulting helps firms and agencies build AI-integrated financial compliance that actually works for the humans using it.Book a consultation

AA

Dr. Ammar M. Ashour, DBA Candidate

Partner & CEO, A&A Tax Consulting LLC · 25 years of tax and financial consulting

Ammar leads A&A Tax Consulting out of Orange, California, where the firm delivers tax preparation, grant accounting, financial statement preparation, and AI-integrated financial compliance services to small businesses, high-net-worth individuals, and government contracting clients. He is completing his doctoral dissertation at California Southern University on reskilling accounting professionals for the AI era.

Key References

- Alhazmi, A. A., & Kaufmann, A. (2022). Phenomenological qualitative methods applied to the analysis of cross-cultural experience in novel educational social contexts. Frontiers in Psychology, 13, Article 785134.

- Braun, V., & Clarke, V. (2022). Thematic analysis: A practical guide. Sage.

- Braun, V., & Clarke, V. (2023). Toward good practice in thematic analysis: Avoiding common problems and be(com)ing a knowing researcher. International Journal of Transgender Health, 24(1), 1–6.

- Choi, J., & Xie, S. (2025). Generative AI in the accounting profession: Evidence from field interviews. Accounting Horizons, 39(2), 45–72.

- Creswell, J. W., & Creswell, J. D. (2023). Research design: Qualitative, quantitative, and mixed methods approaches (6th ed.). Sage.

- Gerhart, B., & Feng, J. (2021). The resource-based view of the firm, human resources, and human capital: Progress and prospects. Journal of Management, 47(7), 1796–1819.

- Johnson, R. B. (2025). A failure to converge? The use of convergent designs in mixed methods research. International Journal of Social Research Methodology. Advance online publication.

- Kokina, J., Blanchette, S., Davenport, T. H., & Pachamanova, D. (2025). Challenges and opportunities for artificial intelligence in auditing: Evidence from the field. International Journal of Accounting Information Systems, 56, Article 100734.

- Tiron-Tudor, A., Deliu, D., Farcane, N., & Dontu, A. (2025). Reskilling accountants for the artificial intelligence era. Journal of Accounting Education, 70, Article 100907.

- van Manen, M. (2021). Doing phenomenological research and writing. Qualitative Health Research, 31(6), 1069–1082.

Dr. Ammar M. Ashour, DBA Candidate · Partner & CEO, A&A Tax Consulting LLC

297 N State College Blvd, Orange, CA · draashour.com

© 2026 A&A Tax Consulting LLC. All rights reserved.

Leave a comment